The modern American experience is defined by a very specific, recurring moment of vertigo that occurs standing in the aisle of a fluorescent-lit grocery store. You are holding a box of cereal, a product made of corn dust and sugar that costs pennies to manufacture, and you are staring at a price tag that suggests the box contains a small semiconductor or perhaps a vial of rare earth minerals. It is eight dollars. You look at the eggs, which have fluctuated in price with the volatility of a meme stock. You look at the beef, which is now priced like a luxury import. And in that moment, you feel the distinct sensation of being mugged in slow motion by an entity you cannot see, touch, or prosecute.

This feeling is the defining political and emotional reality of our time. It is the source of the ambient rage that hums beneath every conversation about the future. We are told, repeatedly and loudly, that this pain is the result of a mystical curse called “Bidenflation,” a narrative that posits the President of the United States possesses a large dial on his desk labeled “Make Things Expensive” and that he turned it to the right for fun. But this is a bedtime story for people who prefer their villains simple and their economics illiterate. The truth is far messier, far more structural, and infinitely more infuriating. The rise in prices did not come from a single policy failure. It came from a catastrophic chain reaction that broke the world, followed by a ruthless corporate looting spree that has successfully rebranded greed as “market forces.”

To understand why your rent is impossible and your sandwich costs twenty dollars, we have to rewind the tape to the moment the world stopped. The pandemic was not just a health crisis. It was a global economic seizure. We took the most complex machine in human history—the global supply chain—and we unplugged it. Factories in China went dark. Ports in Los Angeles froze. Service jobs vanished overnight. We effectively put the global economy in a medically induced coma to save lives, and when we tried to wake it up, we discovered that the patient had forgotten how to walk.

The shock was immediate and violent. Panic buying stripped the shelves. The “just-in-time” inventory system, which prioritized efficiency over resilience, collapsed the moment a single gear slipped. Shipping containers ended up on the wrong side of the ocean. Computer chips, the brains of everything from cars to toasters, were backordered for months. At the same time, the government did the only thing it could to prevent a second Great Depression: it printed money. The stimulus checks were not a socialist plot to devalue the dollar. They were a tourniquet. They kept millions of people from starving and thousands of small businesses from evaporating.

But then came the reopening. It was a chaotic, lurching restart where everyone on the planet suddenly decided they needed the same handful of products at the exact same time. Demand skyrocketed while supply was still putting its shoes on. This is the textbook definition of inflation: too much money chasing too few goods. It was a mechanical inevitability, a consequence of restarting a stalled engine, not a policy choice made in the Oval Office.

The Biden administration, for its part, spent the better part of four years playing whack-a-mole with these crises. They unclogged the ports, running them 24/7 to move the backlog. They released oil from the strategic reserve to temper the insanity at the gas pump. They pushed a vaccination campaign that allowed the labor force to return to work without dying in droves. They boosted competition enforcement to try and break the stranglehold of monopolies. And crucially, they avoided the austerity trap. They refused to jack up interest rates so high that it would have thrown millions of people out of work to “cool” the economy, a strategy that solves inflation by making everyone too poor to buy anything.

And it worked, technically. Inflation cooled. The rate of price increases slowed down. But this brings us to the most painful lesson in economics, the one that politicians hate to explain because it sounds like a surrender. When economists say inflation is “down,” they do not mean prices are going back to 2019 levels. They mean prices are stopping their exponential climb. In the history of modern economics, prices almost never go back down. Deflation is a rare and dangerous beast that usually signals a total economic collapse. What we have instead is a new floor. The price of the ticket has gone up, and it is never coming back down. We are living on a permanent staircase to a more expensive life.

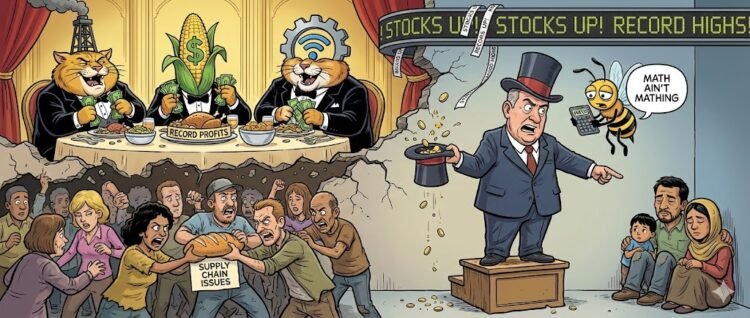

This is where the narrative shifts from “global accident” to “premeditated robbery.” The initial spike in prices was a supply shock. But the persistence of those prices? That is corporate greed, pure and simple. It is the result of a phenomenon known as price stickiness, weaponized by a boardroom class that realized the pandemic gave them the perfect alibi.

For years, companies were terrified of raising prices. They feared consumer backlash. They feared competition. But when the news was filled with stories about “supply chain hell” and “labor shortages,” these corporations realized they had cover. They could jack up prices by twenty percent, blame it on the cost of shipping a container from Shanghai, and the consumer would grumble but pay it. They discovered that the American consumer has a high pain tolerance when they believe the pain is inevitable.

So they raised prices. They raised them to cover their increased costs, and then they raised them a little more. And then a little more. They expanded their profit margins under the guise of survival. And here is the smoking gun: when the shipping lanes unclogged, when the price of fuel dropped, when the cost of raw materials normalized, the prices on the shelf did not move.

Why would they? If you are a CEO and you discover that people will pay six dollars for a carton of eggs, why on earth would you voluntarily lower the price back to three dollars? You wouldn’t. Your shareholders would sue you. Your bonus is tied to margins. You have discovered a new price anchor, and you are going to hold onto it with both hands. The “supply chain” excuse evaporated, but the price tag remained, a monument to the fact that in an oligopoly, the customer is always wrong.

This dynamic is visible everywhere. Look at the rental market. Landlords saw a spike in demand and used “market rates” as a justification to hike rents by thirty or forty percent in some cities. The cost of maintaining the building did not go up by forty percent. The mortgage did not go up by forty percent. The rent went up because they could get away with it. They realized that housing is not optional, and they squeezed the tenant until they could see the bone.

Look at the fast-food industry. We are seeing the death of the “value menu,” a cultural institution that once allowed a person to eat lunch for five dollars. Now, a fast-food meal for a family of four costs as much as a sit-down dinner used to. The companies blame labor costs. They scream that paying a worker fifteen dollars an hour forces them to charge twenty dollars for a burger. But the math does not hold up. In Europe, where wages are higher and benefits are mandated, the same burger costs less. The difference is not the labor; the difference is the profit expectation. The difference is that American corporations have decided that the purpose of a business is not to provide a service, but to extract the maximum possible amount of wealth from the consumer before they break.

This brings us to the most dangerous part of the equation: the wage story. Inflation is a thief, but it steals differently depending on where you stand. For the wealthy, inflation is an annoyance. For the asset class, it can even be a boon, inflating the value of their real estate and their stock portfolios. But for the working class, inflation is a pay cut.

While the cost of living has sprinted up the stairs, wages have been taking the elevator, and the elevator is broken. For most workers, pay increases have not kept pace with the rise in prices. This means that in real terms, most Americans are poorer today than they were four years ago. They are working the same hours, or more, and buying less.

This gap has forced a structural shift in how people survive. We have become a nation of side hustles. The “gig economy” is not a liberation; it is a desperation. Millions of Americans are working a full-time job and then driving Uber, or delivering food, or selling plasma, just to cover the spread between their paycheck and their rent. We are seeing the explosion of “Buy Now, Pay Later” services for basic necessities. People are financing groceries. They are paying interest on a pizza. This is not a sign of a healthy economy; it is a sign of a population that is drowning in slow motion.

Meanwhile, at the top of the pyramid, the party has never been louder. Corporate earnings are hitting records. Stock buybacks—the practice of a company using its profits to buy its own shares to artificially inflate the price—are showering cash on the investor class. This is money that could have been used to lower prices. It could have been used to raise wages. Instead, it was used to enrich the people who already own the company.

CEO pay has skyrocketed to hundreds of times what the average employee earns. We are watching a looting in progress. The wealth generated by the hyper-productive American worker is being siphoned off at the top, leaving the workers themselves to fight over crumbs.

This is not a tidy left-versus-right food fight. It is a lopsided brawl between the top one percent and everyone else. And the brilliance of the system is that both political parties are complicit in the gaslighting. The Democrats point to the stock market and the low unemployment rate and say, “The economy is strong!” They point to the GDP and tell you that you should be happy. But you cannot eat the GDP. You cannot live in the unemployment rate.

The Republicans, for their part, scream about “Bidenflation” while voting against every measure that would actually curb corporate power. They vote against price-gouging bills. They vote against unions. They vote against tax increases on the very corporations that are robbing their constituents. They use the pain of inflation as a political cudgel, but their only solution is to cut taxes for the people causing the pain.

And this leads us to the grand con that keeps the scam running. How do you keep a population from revolting when you are picking their pockets in broad daylight? You give them someone else to blame.

The American media and political culture is a finely tuned machine designed to tell the struggling family in the 80th percentile that their real enemy is the family in the 10th percentile. We are bombarded with narratives about “welfare queens,” about people buying steak with food stamps, about immigrants coming to take our jobs and drain our resources. We are told that the reason our taxes are high is because of social programs, not because of corporate subsidies.

It is a distraction strategy of immense power. It channels the righteous anger of the working class downward. It makes the mechanic angry at the barista. It makes the office worker angry at the migrant picking fruit. It turns the victims of the economy against each other, creating a circular firing squad of the proletariat.

While we are busy arguing about whether a desperate family at the border deserves a tent, the boardroom is quiet. The tax code is being rewritten in the dark. The pricing meetings are happening behind closed doors. A small group of winners is quietly dividing up the gains of a twenty-seven trillion dollar economy, secure in the knowledge that as long as we are fighting a culture war, we will never fight a class war.

We are told to be grateful that the economy looks great on paper. We are told that the “fundamentals” are sound. But the fundamental truth is that an economy that works for the shareholders but fails the workers is not an economy; it is a racket. It is a system where efficiency is measured by how little you can pay someone and how much you can charge them.

The rise in prices is not a temporary bump. It is a permanent restructuring of the social contract. We have moved from a society that valued stability to a society that values extraction. The “supply chain” was fixed years ago, but the prices stayed up because the power dynamic shifted. The corporations realized that they have the leverage, and they are not going to give it back voluntarily.

So the next time you are standing in that grocery aisle, staring at the eight-dollar cereal, do not blame the curse. Do not blame the stimulus check. Blame the business model. Blame the lack of competition. Blame the system that decided that your hunger is a profit center. And realize that the only way the price comes down is not by waiting for the market to correct itself, but by breaking the monopolies that have rigged the market against you.

Receipt Time: The Price of Silence

The most insidious part of this new economic reality is the silence it demands. We are expected to absorb these costs without complaint. We are expected to normalize the idea that survival is a luxury item. When we accept the six-dollar eggs, we are validating the strategy. We are telling them that they won. The “soft landing” the Federal Reserve celebrates is a landing on the backs of the working poor. The inflation was tamed, but the inequality was cemented. We avoided a recession, but we locked in a depression of the spirit, a weary acceptance that in the richest country on earth, you have to work until you die just to keep the lights on. That is not a victory. That is a surrender.