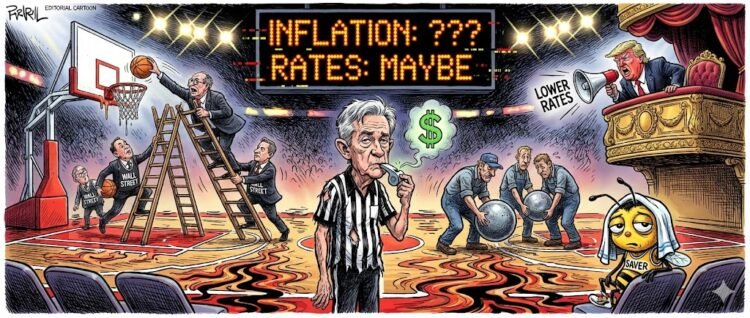

Jerome Powell is the tired referee in a game where the scoreboard is broken, the players are cheating, and the owner is screaming from the luxury box to let the home team win or else.

If you want to understand the current state of the American economy, you do not need to look at a yield curve or parse the minutes of the Federal Open Market Committee. You simply need to imagine a high school basketball game officiated by a referee who has not slept in three days. The scoreboard is flickering between random numbers. One team is openly traveling on every possession while the other is deflating the ball. And in the stands, the team owner—let’s call him the President—is running onto the court screaming that the basket should be lowered by two feet immediately because he likes seeing dunks. In the middle of this chaos, the referee blows his whistle, awards a single free throw, and whispers that he might call a foul again next year, maybe, if he feels like it. This is essentially what the Federal Reserve did on Wednesday.

In a move that managed to confuse everyone while pleasing absolutely no one, the central bank cut interest rates by a quarter point, bringing the target range down to 3.5 to 3.75 percent. It was the third straight cut. It should have been a victory lap. Instead, it felt like a hostage video. The vote was nine to three, the most internal dissent the Fed has seen in years. Two members voted against the cut entirely, arguing that inflation is still a beast waiting in the tall grass. One member voted for a bigger cut, presumably because they looked at the labor market and saw a cliff edge. And Jerome Powell, the man tasked with threading this impossible needle, stood at the podium and insisted that everything is fine, that they are “recalibrating,” and that we should all expect exactly one lonely rate cut in 2026.

We are witnessing the birth of the “hawkish cut,” a new genre of monetary policy that feels like a parent handing their teenager a credit card while simultaneously delivering a forty-minute lecture on the virtues of austerity. The Fed is giving the market the cheap money it craves, but it is doing so with a scowl. They are easing off the brake, but they are refusing to touch the gas. It is a policy designed to maximize cognitive dissonance. We are told that inflation is easing but not beaten. We are told the labor market is cooling but not collapsing. We are told that financial markets are frothy, stock indices are popping, and bond yields are sliding, yet somehow we still need to stimulate the economy just a little bit more.

The contradictions are enough to give a rational observer a migraine. Core inflation is still stuck around 2.8 percent, which is significantly higher than the Fed’s sacred two percent target. Unemployment is drifting higher, creeping up in a way that usually signals a recession is waving from the driveway. GDP growth forecasts have been nudged up to about 2.3 percent next year, suggesting an economy that is doing just fine. And yet, here we are, cutting rates. It is like taking antibiotics for a cold you aren’t sure you have, just in case the doctor thinks you look pale.

The reality is that the Fed is flying blind. Thanks to government shutdown delays and the general degradation of federal data gathering, the economic picture is patchy at best. They are landing a 747 in a fog bank, relying on instruments that haven’t been calibrated since the last crisis. And sitting in the cockpit, Jerome Powell is trying to project a calm “glide path” into 2026 while the proximity alarms are blaring in the background.

The Dysfunctional Family Thanksgiving at the FOMC

To understand the decision, you have to look at the people making it. The Federal Open Market Committee has turned into a dysfunctional family dinner where everyone is shouting past each other. The doves are terrified of layoffs. They look at the “cooling” labor market and see the ghosts of 2008. They see hiring freezes. They see the hollowing out of the federal workforce. They want to cut rates now, fast and deep, to save the jobs that are barely hanging on.

The hawks are obsessed with price stability. They look at 2.8 percent core inflation and see the ghosts of the 1970s. They see tariffs driving up the cost of goods. They see geopolitical shocks spiking oil prices. They see a federal deficit that is ballooning out of control, fueled by tax cuts and spending that pumps demand into an already hot system. To them, cutting rates now is madness. It is pouring gasoline on a smoldering fire. They voted “no” because they believe the only way to kill inflation is to strangle the economy until it stops moving.

And in the middle, you have the centrists, clinging to the “dot plot” like a security blanket. The dot plot is that famous chart where Fed officials anonymously project where they think rates will be in the future. It is treated by Wall Street pundits with the reverence of a holy text, but in reality, it is more like a horoscope for hedge fund managers. “Your 2026 holds one cut,” the chart says, “but beware of persistent core services inflation and unexpected trade wars.” It is a work of fiction. It is a collective guess made by twelve people who have been wrong about almost every major economic shift of the last decade.

The statement they released reflects this paralysis. It says they will cut once next year. The market, of course, does not believe them. The market is already pricing in more easing, turning every phrase of Powell’s press conference into a Rorschach test. If he coughs, traders buy bonds. If he smiles, they sell dollars. They know that the Fed is reactive, not proactive. They know that if the economy stumbles, the “one cut” promise will vanish faster than a campaign pledge after election day.

The specter looming over the entire proceedings is, of course, Donald Trump. The President is not content to let the independent central bank do its job. He is on the sidelines, raging that the cut is too small. He demands a double-size move. He wants zero percent rates because zero percent rates make the stock market go up, and the stock market is the only poll he cares about. He is publicly auditioning new Fed chairs based on who promises the deepest future cuts, turning monetary policy into a reality TV competition.

This politicization of the Fed is the quiet nightmare behind the numbers. The central bank is supposed to be the adult in the room. It is supposed to take away the punch bowl just as the party gets going. But Trump wants a bartender who pours shots until everyone passes out. He views the Fed as just another cabinet department waiting to be “fixed,” another lever of power to be pulled for short-term gain. And Powell knows this. He knows that every decision he makes is being judged not just by economic data, but by a President who views “independence” as a synonym for “disloyalty.”

So we get the compromise. We get the quarter-point cut. We get the “hawkish” language. It is an attempt to appease the market without spooking the inflation hawks, to stimulate growth without triggering a presidential tantrum. It is a policy made of fear. It is the action of a committee that is terrified of making a mistake, so they make the smallest possible move and hope nobody notices that they don’t have a map.

The View from the Checkout Line

While the pundits debate basis points and the bond market celebrates, the view from the ground is very different. For real people, this rate cut is a rumor. It is a headline they see on their phone while they are standing in line at Walmart, staring at a grocery total that makes them want to weep.

Mortgage borrowers are still waiting. A quarter-point cut in the federal funds rate does not immediately translate to 3 percent mortgages. Rates are still high. Refinancing is still a pipe dream for millions of families locked into homes they can no longer afford to leave. The housing market remains frozen, a game of musical chairs where the music stopped three years ago and everyone is just standing around staring at the empty seats.

Credit card users are drowning. APRs are still north of 20 percent. A quarter-point cut is mathematically irrelevant when you are paying 24 percent interest on the groceries you bought last month. The debt trap is real, and the Fed’s “gradual adjustment” does nothing to open the jaws. It is like tossing a thimble of water to someone dying of thirst in the desert. It is technically help, but it feels like an insult.

Small businesses are facing expensive credit lines that make expansion impossible. The cost of capital is still prohibitive for the local bakery or the independent contractor. They are being squeezed by inflation on one side and high interest rates on the other. They see the stock market booming, driven by AI investments and massive data center projects, and they wonder what economy the news is talking about. The windfall is going to the giants. The crumbs are falling to the rest.

Renters never see “rate cuts.” Rent only goes up. It is a law of physics in the modern economy. The landlord’s variable rate mortgage might get a tiny bit cheaper, but he isn’t passing that savings on to you. He is raising the rent because the market says he can. The affordability crisis is not a monetary phenomenon; it is a structural failure. And the Fed has no tools to fix it.

Savers, the few who are left, see their meager interest income shrink again. The brief window where you could earn 5 percent on a savings account is closing. The message from the Fed is clear: Stop saving. Go spend. Go buy stocks. Go gamble. The economy needs your consumption, not your prudence.

Powell talks calmly of “threading the needle” and “soft landings.” But families at Aldi do their own inflation expectations. They look at the price of eggs. They look at the price of insurance. They look at the shrinking size of the cereal box. They know that “2.8 percent inflation” is a statistical abstraction. The cumulative effect of years of price hikes means that life is simply more expensive, permanently. The prices aren’t going back down. The rate of increase is just slowing. That is not relief. That is just a slower form of drowning.

The larger political economy is feeding this fire. Tariffs are driving up costs. When we tax imports, we tax ourselves. The consumer pays the price. The federal deficit is pumping money into the system, keeping demand high even as the Fed tries to cool it. It is a tug-of-war where the rope is the American middle class. The government steps on the gas with spending and tariffs; the Fed steps on the brake with rates. The result is an engine that screams and a car that goes nowhere.

We have to ask whose side monetary policy is really on. If the Fed is cutting because growth is fragile and the labor market is weakening, why do they refuse to promise more help? Why do they insist inflation is still too high while cutting rates anyway? It feels like they are managing the stock market, not the economy. They are terrified of a crash. They are terrified of the wealth effect evaporating. So they hand out the cuts to keep the line moving up and to the right.

The central bank has become the nervous hall monitor of a system that is fundamentally broken. It keeps handing windfalls to the markets while telling workers to be patient. “Wait for wages to catch up,” they say. “Wait for prices to stabilize.” But the wait is over. The patience is gone.

Three small cuts and a promised pause are not a cure for stagflation risk. They are a way of buying time. They are a way of kicking the can down the road until after the next election, or until the next crisis forces their hand. They are praying that the AI boom is real, that productivity will save us, that the tariffs won’t start a global trade war. They are betting the house on a hand they haven’t looked at yet.

In this economy, the only thing truly low and stable is trust. Trust in the institutions. Trust in the data. Trust in the people holding the interest rate lever. We look at the referee, sweating and blowing his whistle, and we realize he doesn’t control the game anymore. He is just watching it happen, hoping the owner doesn’t fire him before the clock runs out. And the rest of us are just trying to afford a ticket to the cheap seats, watching the scoreboard glitch, wondering when the game became so rigged that even winning feels like losing.