When politicians hand you a debit card instead of a health system, and call it innovation

There is a special place in the American imagination where problems do not need solutions, they only need branding. Bridges do not need maintenance, they need ribbon cuttings. Schools do not need funding, they need mascots. And health care does not need insurance, regulation, or affordability, it needs a shiny debit card with a name like FreedomFlex or LibertyHealth or PatriotCare Ultra Max.

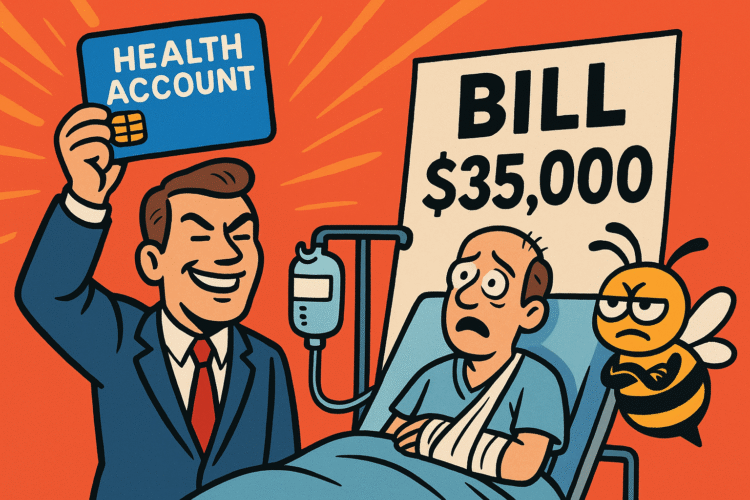

This is the political sleight of hand known as the health account. The idea that instead of giving you actual health care protections, policymakers can hand you a plastic card, sprinkle some talking points on top, and pretend they have reinvented medicine. They tell you these accounts empower you. They tell you they put you in charge. They tell you freedom means shopping around for your own chemotherapy like you are comparing flights to Phoenix.

But when you translate the vibes into math, the whole fantasy collapses. Not gracefully. Not elegantly. It collapses the way a folding chair collapses under the weight of a man who insists physics is a personal conspiracy.

Let us begin in the emergency room. No one comparison shops during an emergency because no one wants to die in a parking lot while Googling “cheapest broken arm X ray.” Real life does not care how empowered your debit card feels.

A simple broken arm can land you in the low thousands before you even get the cast. Imaging, urgent care, immobilization, physician fees, the follow up visit where they ask if you’ve been keeping weight off of it even though you clearly have not. If the arm needs surgical repair, it is five figures. That is not hyperbole. That is Tuesday. Try swiping your health account on that and watch it flinch like a smoke alarm sensing humidity.

Pneumonia? You are in the five to mid five figures depending on length of stay. A heart attack? Tens of thousands once the cath lab rolls you in, balloons a vessel open, and you spend a night in the ICU listening to monitors beep out their own existential anxiety. Cancer? Cancer is not a bill. Cancer is a season of bills. Chemotherapy alone can run thousands to tens of thousands per month depending on the regimen. Radiation has its own tab. Imaging has its own tab. Labs have their own tab. Your wallet becomes a subscription service to the concept of staying alive.

This is where the health account fantasy dissolves. Not gradually. Instantly. Because no realistic account balance touches these numbers. Not unless you are already wealthy, which is the political twist ending they hope you never notice.

To prove the absurdity, let us go line by line through the charges health accounts are supposedly designed to encourage you to shop for.

A unit of blood, once transfused, becomes roughly a thousand dollars. Saline, literal salt water in a bag, becomes a triple digit charge. The average emergency room visit hovers in the low thousands long before anything serious happens. You can walk into an ER with chest pain, walk out with indigestion, and still owe a number large enough to buy a used car.

And none of this includes the “innovation” health accounts never provide. Preexisting condition protections? Gone. Community rating to keep premiums stable? Gone. Essential health benefits? Gone. Out of pocket caps? Gone. Surprise billing protections? Gone. Instead you get market discipline, which in health care means a patient in a gown trying to comparison shop a CT scan while struggling to breathe.

The math is cruel. The ideology is crueler. A health account without robust insurance is not empowerment. It is a staged reenactment of financial independence where the actors forget to tell you the ending ends badly.

Politicians sell these accounts as disruption. They call them modern. They call them consumer driven. But consumer driven care in America is code for “blame the patient when they cannot afford it.” It is the perfect libertarian fantasy where no one owes anyone anything except their own ruin.

And let us be clear. This is not a theoretical harm. This is a real world, receipt level, “why is the bill for saline the size of a utility payment” harm.

The winners in this system are not patients. The winners are medical debt securitizers, boutique administrators, and lenders who earn fees off your misfortune the way casinos earn revenue off the chronically unlucky. They turn human illness into a financial product. They sell your emergencies to each other the way traders sell futures contracts.

Meanwhile households absorb the damage. Deductibles reset every year like a seasonal allergy. Coinsurance pops up like pop up ads you cannot block. Out of pocket costs become a second rent payment. You are maintaining your own body the way you maintain a home that keeps aging without your consent.

You become a fifty year style liability to yourself.

And at the macro level, the game becomes even clearer. Health accounts subsidize demand without fixing supply. They give people the illusion of affordability but no actual affordability. Prices rise. Providers charge more. Insurers recalibrate. Hospitals recoup losses with higher commercial rates. Renters are crowded out. The uninsured spiral deeper. And uncompensated care returns to emergency rooms that pass the costs to everyone else.

Nothing about this model is innovative. It is cost shifting disguised as freedom.

And if you want to see how the shell game works, look for the pieces they never mention. They never mention total cost of care tables. They never publish comparisons between a high deductible plan with a health account versus comprehensive coverage for a heart attack or a cancer regimen. They never mention what happens when the account runs dry. They never mention that an ATM is not health insurance, no matter how patriotic the branding on the card may look.

A system built on health accounts without statutory rights is a horror story told quietly enough that people think it is policy.

The checkpoints for separating marketing from medicine are simple. Does the proposal include guaranteed issue protections? Does it include community rating? Does it preserve essential health benefits? Does it enforce out of pocket caps? Does it extend surprise billing protections? Does it cap premiums? Does it regulate junk plans pretending to be real insurance?

And the most important question of all: can the account survive real medical math?

If the answer is no, then it is not health care. It is a payment mechanism designed to collapse under its own optimism the first time someone needs more than a wellness visit.

A politician holding up a debit card and calling it health care is like a magician sawing an assistant in half and claiming he has improved outpatient surgery. It looks impressive until someone needs actual medical care. It dazzles until the first real bill lands. It works until it doesn’t, which in American health care means it does not work at all.

A health account without real insurance is an idea designed to appeal to people who have never had a medical crisis, never seen an ambulance bill, never waited for pathology results, never signed a consent form in a fluorescent hallway, never felt their stomach drop at the sound of the words your portion.

This is not innovation. It is austerity with better lighting.

And the sooner the press stops treating it like a new frontier in consumer choice and starts printing the truth in plain English, the better.

A health account without comprehensive coverage is not a solution. It is an ATM that runs out the instant real medicine begins.