Translate the slogan into math and law, and the promise to “send the money to the people” becomes a coupon for chaos with the patient protections ripped off the box.

The pitch sounds generous if you hear it from far away. Cut out the insurance companies, send the money straight to you, terminate the bad program that annoys a certain president when he sees the name. From distance, it reads like a populist refund. Up close, it is a rental car with no brakes. The idea is not new. It takes the same dollars that buy regulated coverage today and tries to rebadge them as freedom bucks you can spend on whatever qualifies as a health plan once the rules that made a plan a plan are gone. The translation is simple. Replace statutes with vibes. Call it direct. Pretend the middleman is out of the picture while the only sellers left are the same middlemen, now unburdened by the protections that made them tolerable.

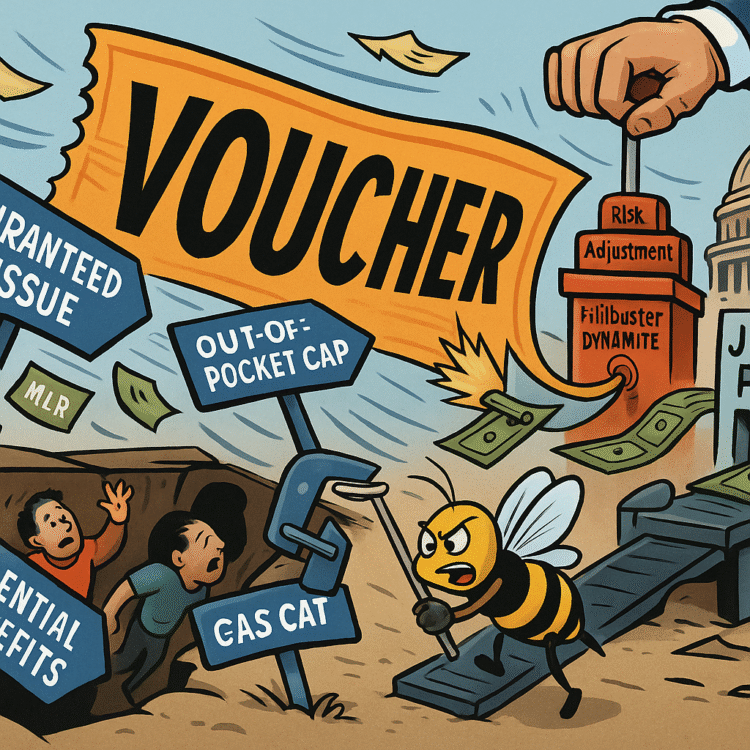

Let us do the arithmetic the pitch avoids. The “hundreds of billions” he waves at are not loose coins in a couch. They are specific, boring transfers that already land in households and providers in ways that can be traced. Premium tax credits reduce monthly premiums for people who buy on the exchanges. Cost sharing reductions cut deductibles and copays for lower income enrollees. Medicaid expansion brings in federal matching dollars at a rate that makes budgets breathe. Risk adjustment moves funds from plans with healthier enrollees to plans with sicker ones, so no one wins by cherry picking. Reinsurance programs keep the highest claims from detonating premiums for everyone else. Medical loss ratio rules force insurers to spend most premium dollars on care and quality improvement, with rebate checks mailed back when they fall short. These are not rumors. They are line items and checks with names on them.

Now put the slogan next to the statute. “Terminate Obamacare” means erase the guardrails that make those dollars purchase something that works for a human body. Guaranteed issue is the rule that says a plan cannot turn you away. Community rating is the rule that says they cannot price you like a luxury car because you once had cancer. Essential health benefits are the floors under what must be covered, from hospitalization to maternity care to mental health to prescription drugs. Out of pocket caps stop a bad year from becoming a bankruptcy by limiting total cost sharing. The rule that lets a 26 year old stay on a parent plan is not a kindness. It is a safety policy that cushions the most volatile years. The 80 to 85 percent medical loss ratio prevents an insurer from converting premiums into yachts. Rate review makes price hikes justify themselves to adults. Network adequacy rules keep a plan from being a map of specialists you cannot find. Surprise billing limits stop an emergency from becoming a financial ambush.

If you convert the money into “vibes vouchers” while terminating the statute, you do not remove the middleman. You remove the traffic laws and leave the drivers. The only sellers left are the same companies, now free to resurrect junk plans that whisper promises and speak exclusions. The patient protections are gone, but the market power remains. The result is not freedom. It is the return of medical underwriting, lifetime caps, preexisting denials, and benefit schedules engineered to collapse exactly when a body is expensive. That is not a theory. It is the history we lived before the current rules existed.

The math gets worse when you model behavior. If you hand out cashlike subsidies with fewer strings, healthy people have every incentive to roll the dice on skinny coverage or to wait. Sick people will buy the richest product they can find. That is textbook adverse selection. Premiums spike for those who actually need coverage because the risk pool tilts toward higher cost. In response, plans either raise prices for real insurance or they design products that look like insurance and break on contact. The slogan says cut out the middleman. The ledger says you cut out risk adjustment and community rating and the rest of us pay for the fun.

Consider the legal plumbing that keeps the current ecosystem from eating itself. Risk adjustment stabilizes the pool by moving dollars from plans with healthier members to plans with sicker ones. Without it, one company wins by courting marathon runners and ghosting diabetics. Reinsurance keeps a handful of catastrophic claims from detonating next year’s rates. Without it, the insurer who had a bad year punishes every new customer for the sins of a few. Rate review lets regulators say no to increases that are more about margin than medical trend. Without it, the answer to every cost surge is a letter with a larger number. Surprise billing protections keep a patient from being trapped between a broken network and a bill collector. Without them, a visit to the wrong emergency room turns into a lien on a car. Medical loss ratio rebates put real money back in pockets when an insurer spends too little on care. Without them, the premium becomes a profit reservoir.

The Medicaid side of the ledger is not a footnote. The federal match for expansion made it possible to cover millions of low wage workers in jobs that never offered benefits, while stabilizing hospital finances in places where uncompensated care was an annual hemorrhage. Voucherizing Medicaid means handing out cards that buy less in markets where plans can refuse to contract with the providers people actually use, or it means pushing people toward short term products that exclude the very services poor and disabled enrollees need most. The fantasy is that cash is flexibility. The reality is that flexibility without rules is rationing by wallet.

Now count the pieces that already flow back to real people. Premium tax credits do not go to insurance companies as a tip. They reduce what a family pays each month, at the point of sale. Cost sharing reductions do not fund corporate retreats. They lower the deductible for a person who will otherwise delay care. Medical loss ratio rebates are checks addressed to households and small employers because an insurer failed to meet a spending threshold on care. Reinsurance prevents the premium spike that would have eaten your raise. FMAP dollars for Medicaid expansion keep a state budget from gutting classrooms to pay hospital bills. The current system is not a romance. It is a series of negotiated constraints that force private actors to behave like participants in a public project. Replace that with cash cards and a shredded statute, and you do not create a new kind of freedom. You create a new kind of exposure.

Let us make the consequences plain, because this is not a seminar. Adverse selection arrives fast. Healthier people take the voucher and either buy the thinnest product or buy nothing until a knee buckles or a scan lights up. Premiums for comprehensive plans rise because the risk pool sours. Junk plans flood the market with exclusions, waiting periods, and benefit caps that read like a dare. Medical underwriting returns, which means you will be asked to recall every diagnosis and denial you have ever had, and an algorithm will decide whether you are profitable enough to cover. Lifetime and annual caps reappear with cute branding. Essential health benefits sunset, so maternity care, mental health treatment, and prescription drugs become optional riders in a country where most people cannot afford a surprise bill. Preventive services without cost sharing vanish, so contraception and cancer screening become line items families postpone. Surprise bills walk back in the front door because the statutory shield is gone. State regulators scramble to plug holes with waivers. Lawsuits bloom. Hospitals, now eating more uncompensated care, shift the costs to paying patients and employers. The system finds a new equilibrium by pushing more risk to households that already do not have cushion.

The sales job will lean hard on language. Politicians will call subsidies “direct cash to families” while omitting that the statute that made those subsidies worth something has been torched. They will call network rules “bureaucracy” and medical loss ratio “red tape.” They will say the market can police itself while privately calling lobbyists to make sure the rules that remain are soft. They will invoke choice while designing products that collapse the first time choice meets illness. They will call this deregulation “freedom.” They will not say which actors are now free to deny, exclude, and overprice. You can infer the answer by checking who wrote the draft.

There is a civics kicker baked in, and it deserves to be said in plain English. He is not just promising to mail out vibes vouchers. He is blowing a kiss to the idea of scrapping Senate Rule 22, the filibuster, to do it. A bare majority could then voucherize Medicaid, defund cost sharing reductions, sunset essential health benefits, neuter risk adjustment, and tinker with medical loss ratio in a single reconciliation push dressed up as relief. You would wake up in a country where the entire architecture of regulated private coverage was swapped for cash cards and a trust me. The pitch will call it cutting out the middleman. The result is cutting out the protections while leaving the middleman with a wider smile.

The defenders will try a few familiar moves. They will say that states can build their own protections. Some will try, many will fail, and the postal code lottery will get crueler. They will say that employer coverage will continue to be strong. They will omit the part where employer plans face fewer guardrails when federal floors are gone, and where the next downturn gives companies an excuse to slash benefits and shift costs. They will say that health care is too complex for Washington. That argument arrives every time someone wants to deregulate a market and keep the subsidy. Complexity is not a reason to abandon rules. It is a reason to write them clearly.

If you want receipts, here is what the current framework already does on autopilot. If an insurer spends less than the required percentage of premiums on care and quality, you get a rebate check. If a plan proposes a rate hike that is out of line with trend, regulators can push back. If you get hit by a car and wake up in an out of network emergency room, the law steps between you and a predatory bill. If you are twenty three and broke, you can stay on a parent plan and finish school without taking out a loan to pay an MRI. If you have a chronic condition, you can apply for coverage without rehearsing your medical history like a confession. If you get pregnant, the policy recognizes pregnancy as a normal part of human life, not an add on for people who can afford it. These are tangible, boring protections that do not care about your politics. They care that you are a person.

There is a reason the voucher pitch has to be loud. It only works if people forget what the rules do. It has to pretend that cutting insurers out is the goal when the actual product leaves insurers right where they are, relieved of obligations and flush with new options to sell fantasy. It has to portray regulators as villains to distract from the fact that, without them, the market does what markets do when profit can be increased by shedding the expensive. It has to rename subsidies as cash because cash tests well and statutes do not. It has to package a deregulatory wish list as a raise for families, while families will discover that the raise buys less each time a clause returns from the past.

The health system is not a single market. It is a network of incentives where failure in one corner makes everyone else pay. Medicaid cuts increase hospital bad debt. Hospital bad debt pressures commercial rates. Commercial rate pressure raises premiums and deductibles. Higher cost sharing forces people to skip care. Skipped care turns small problems into expensive emergencies. Expensive emergencies flood emergency rooms. Emergency rooms pass costs along. The political class then looks at the growing bill and decides the answer is more vouchers. You can see the loop tighten. You can see who falls through.

There is a more honest version of direct help if that were truly the goal. Keep the statutory protections, expand subsidies where premiums and deductibles still crush, grow reinsurance to blunt regional spikes, enforce medical loss ratio with a spine, police networks so that access exists in the real world, fund navigators so people can actually use the system, and invest in the parts of care delivery that make health less expensive to maintain. That version is boring, measurable, and unpopular with people who prefer ideology to outcomes. It also works.

If your patience for civics is not infinite, here is the part that matters this week. Watch for any draft that tries to rebrand premium support as cash cards while “streamlining” or “sunsetting” the statutory protections that make a plan a plan. Watch for budget texts that quietly neuter risk adjustment or shift its design so gaming becomes the best business model. Watch for reconciliation language that tweaks medical loss ratio thresholds or definitions in ways that let more non care spending pass as quality improvement. Watch for Medicaid language that calls voucher pilots flexibility while capping federal commitments in ways that guarantee rationing. Watch for marketing from new intermediaries who swear they are not insurers, they are platforms, and ask why platforms need to be exempt from rules that protect patients. Watch for a chorus of lobbyists selling deregulation as freedom while the only freedom on offer is for sellers to decide who gets served and at what price.

Also watch the courts, because this crowd prefers to break what they cannot pass. If they fail to legislate, they will litigate the remaining pillars. They will call preventive services a religious liberty problem. They will call network rules a restraint on speech. They will call cost sharing reductions an appropriations question. They will call medical loss ratio a taking. They will shop venues and wait for the right judge. In response, the only defense is relentless enforcement, clean statutory language, and a public that understands what is being taken from them while they are told it is a gift.

The final irony is not subtle. A president who railed against blood sucking insurance companies now proposes a program that leaves those companies with more freedom and less restraint. He wants to cut out the middleman by cutting out the rules that hold the middleman accountable. He wants to send the money to the people by removing the guardrails that ensure the money buys something real. He wants to call it populism while making the purchase of coverage more confusing, more risky, and more dependent on fine print. If you feel like you have heard this before, it is because you have. It never ends well for patients.

Receipts, Not Vibes

The ledger is not complicated. Today’s dollars fund regulated coverage that must take all comers, price without punishment for history, include core benefits, cap out of pocket costs, block surprise bills, move money to where the sick are, and refund customers when insurers underspend on care. Rebrand those dollars as vouchers while terminating the statute, and you buy exclusions, caps, denials, and networks that collapse when someone needs care. The claim that you are cutting out the middleman is theater. You are cutting out the protections and leaving the middleman with more ways to say no. If the plan requires scrapping the filibuster, the agenda is not moderation. It is speed for a demolition. This week, watch for any draft that sells cash cards without statutory floors, any budget text that guts risk adjustment or medical loss ratio, and any lobbying push that calls deregulation freedom. Translate every sentence back into a real life question. If I get sick, who has to take me, what do they have to cover, how much can they make me pay, and what happens when the fine print shows up. If the answer depends on luck, the voucher is a vibe and the bill is yours.