There is a specific, heavy silence that settles over the internet when the gambling stops being fun and starts being mathematical. You can feel it in the sudden drop in laser-eye profile pictures on social media. You can hear it in the absence of “Have Fun Staying Poor” tweets. It is the sound of a bubble hissing as the air leaves the room, replaced by the cold, hard vacuum of realized losses. We are currently living through one of those moments, a historic and brutal faceplant where roughly one, single, solitary trillion dollars in market value has evaporated in about six weeks.

To put that number in perspective, one trillion dollars is not just a statistic. It is the GDP of a mid-sized European nation. It is enough money to solve several global crises. Instead, it was parked in a digital ledger, fueled by memes and low interest rate nostalgia, and now it is gone. It vanished into the ether, taking with it the retirement dreams of retail investors who were told that this time was different.

The autopsy of this crash reveals a body that was never quite as healthy as the evangelists claimed. Bitcoin, the flagship of this volatile armada, has tumbled from its October peak near $126,000 to the low $80,000s. In the span of a few weeks, it has erased all of its 2025 gains. It has logged its worst month since the frozen depths of the 2022 crypto winter. We watched as prices repeatedly knifed below psychological safety nets like $90,000 and $85,000, briefly flirting with $81,000 as if testing the floor to see if it was made of concrete or trapdoors.

This was supposed to be the year of the “Supercycle.” It was supposed to be the era of institutional adoption where the adults in the room—BlackRock, Fidelity, the pension funds—put a floor under the price. Instead, the adults in the room did exactly what adults do in a casino when the fire alarm gets pulled. They ran for the exits, trampling the retail tourists on the way out.

The carnage is not limited to the orange coin. Ether, Solana, XRP, and the rest of the majors have followed the leader down in double-digit declines, dragging the total crypto market cap back under the $3 trillion mark. The wealth effect of early 2025 has been exposed as a hallucination. The Lamborghinis are being returned to the dealership. The “community” is fracturing into recriminations and panic.

The drivers of this collapse, identified by everyone from Reuters and Bloomberg to CoinDesk and Barron’s, are a perfect storm of macro reality colliding with speculative fantasy. The primary catalyst was a sharp swing in macro sentiment. The Federal Reserve, specifically Chair Jerome Powell, issued a “serious” warning. Combined with the delayed and messy jobs data—a statistical void that left traders flying blind—the market realized that interest rate cuts are not coming as soon as hoped. The “money printer go brrr” narrative that fuels crypto bull runs has jammed.

When money is expensive, people stop buying magic beans.

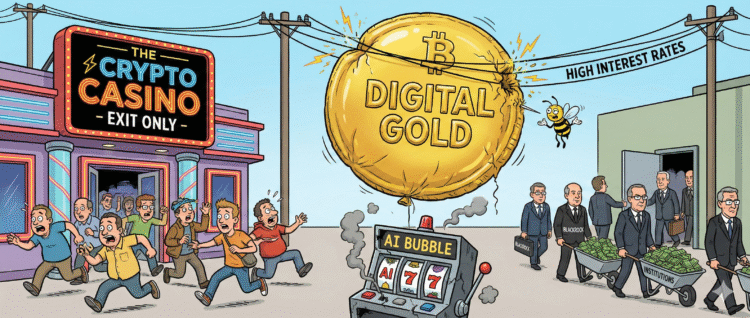

This triggered a broader flight from risk that did not just hammer crypto but also took a baseball bat to the Nvidia-led AI stock rally. This correlation is the most damning piece of evidence against the “Bitcoin is digital gold” thesis. Gold is a hedge against chaos. Gold holds value when the tech sector implodes. Bitcoin, however, acted exactly like a high-beta tech stock strapped to a slot machine. When the AI bubble started to leak, crypto started to crash. It is not a safe haven. It is just another risk asset, trading in lockstep with the most speculative corners of the Nasdaq.

The specific mechanics of the crash were brutal. We witnessed record outflows of roughly $3.7 billion to $3.8 billion from U.S. spot bitcoin ETFs in November alone. These were the vehicles that were supposed to save us. We were told that once BlackRock’s IBIT and the other funds were approved, the supply shock would send prices to the moon. Instead, these funds have been spewing cash. The institutional investors, having made their profit, are rotating out, proving that they have no ideological attachment to “decentralization.” They are mercenaries, and the contract is up.

The exit of the big money triggered a violent cascade of liquidations. An estimated $1.5 billion to $1.7 billion in leveraged long positions were force-sold into a thinning liquidity pool. This is the classic crypto death spiral. Traders borrow money to buy bitcoin, betting it will go up. When it goes down, the exchange automatically sells their bitcoin to pay back the loan. This selling drives the price down further, triggering more automatic sales from other traders. It turns every intraday wobble into a cliff dive. It is a system designed to amplify pain.

The options markets, tracked by platforms like Derive.xyz, now paint a grim picture. They put the odds of bitcoin ending the year below $90,000 at around 50 percent. The optimism has been mathematically exorcised. Analysts at outlets from Business Insider to CBS and Forbes are issuing warnings that the slide is increasingly correlated with a broader AI tech bubble unwind. The story has shifted overnight. Two months ago, every dip was a “healthy correction” on the way to $150,000. Now, experts are debating whether this is a “downward spiral” or the start of a dot-com style comedown.

We are potentially looking at a scenario where a few blue-chip protocols survive, but a lot of retail speculators learn a very expensive lesson about what “volatility” actually means. It does not just mean the price goes up fast. It means the price goes down faster.

The “digital gold” narrative is dead. You cannot call an asset a store of value when it loses thirty percent of its value in a month because Nvidia missed an earnings target or the Bureau of Labor Statistics had a server outage. Gold does not care about GPU sales. Bitcoin cares deeply. It is tethered to the hype cycle of Silicon Valley, not the monetary policy of the central banks. It is an index of liquidity and exuberance, nothing more.

The tragedy is that the people getting hurt the most are not the venture capitalists who got in at $100. It is the regular people who bought in at $120,000 because a podcast host told them they were buying “financial freedom.” They were sold a ticket to a revolution and ended up holding the bag for a correction. They were told to “HODL” by people who were secretly selling.

This is the cyclical nature of the grift. The market pumps, the hype machine engages, the retail money floods in, and then the trap door opens. The $400 billion lost in the last week alone represents tuition payments, down payments on houses, and emergency funds. It represents real human potential wasted on a speculative asset that produces nothing but anxiety.

As we watch the charts bleed red, it is worth remembering that the underlying technology of blockchain has yet to solve a problem that a database couldn’t solve cheaper. The entire ecosystem is a circular economy of tokens trading for other tokens, propped up by the promise that a “greater fool” will come along and pay more. But eventually, you run out of fools.

The shift in tone from the financial press is palpable. The breathless cheerleading has been replaced by somber analysis of “support levels” and “resistance bands.” They are drawing lines on charts as if astrology can explain why the gambling addicts left the casino. The reality is simpler. The easy money is gone. The Fed is not coming to the rescue. And the AI bubble, which provided the draft that crypto was drafting behind, is starting to wobble.

We are witnessing the bursting of the “Everything Bubble.” Crypto was just the most pressurized part of the balloon. It popped first. The question now is not when Bitcoin goes back to $126,000. The question is how many people can get out before it tests $50,000. The “risk-on rocket ship” has run out of fuel, and gravity is a harsh mistress.

The Part They Hope You Miss

The most insidious part of this crash is the silence regarding the “stablecoins.” As the market cap plummets, billions of dollars are fleeing into USDT and USDC, the digital dollars that underpin the entire trade. These entities are unregulated banks operating in the shadows, holding vast amounts of commercial paper and Treasury bills. If the panic spreads to them—if the people fleeing Bitcoin try to redeem their Tethers for actual U.S. dollars and find the window closed—then the $1 trillion loss we just witnessed will look like a rounding error. The structural risk of the crypto ecosystem is not that Bitcoin goes down; it is that the plumbing explodes. The current liquidation cascade is a stress test for a system that has never truly been tested, and the creaking sounds coming from the hull should terrify anyone still on board.